Why and how you should buy T-bills today

Why and how you should buy T-bills today

Take advantage of high interest rates

Hey friends 👋

Today’s newsletter will focus on the less glamorous side of investing - government securities. I am shocked at the number of people I’ve spoken to recently that have their savings sitting in cash waiting for the “right time” to put their money back in the market. With ~0% interest rates for such a long time we’ve forgotten that there are fixed income securities out there that are yielding a pretty decent return. Let’s nip this in the bud.

Bonds are no longer only for Boomers

Ever since I started working back in 2011 interest rates have been close to 0%. With such low interest rates investing in fixed income securities looked far from appealing. Banks were giving a laughable 0.01% interest on savings accounts. Treasury securities were not paying much higher than that. This was obviously no coincidence. After the 2008 financial crisis the Fed reduced interest rates to stimulate the economy. They didn’t want you to keep your money in your savings accounts. They wanted you to spend money to help the economy recover.

Before 2008, however, our Boomer counterparts invested in fixed income securities. Not because they were necessarily risk averse, but more because at pre-2008 interest rate levels it made sense for a part of their investment portfolio to earn fixed, predictable income. The chart below shows the effective fed funds rate between 1979 and today.

Now that interest rates are back up, it makes sense to consider adding bonds to our investment portfolio. This is especially true in the short-term with high short-term interest rates on treasury bills, but is also true in the long-run as the U.S. economy stabilizes at a higher-than-zero interest rate.

Treasury bills should be part of everyone’s portfolio right now

We’re in a time of economic uncertainty. There are plenty of signs of an upcoming recession from an inverted yield curve to leading economic indicators (LEIs). At the same time Jerome Powell’s comment that “disinflation has begun” has been taken as a win by markets. The stock market has never bottomed before the onset of a recession, but this could be a first? Only time will tell.

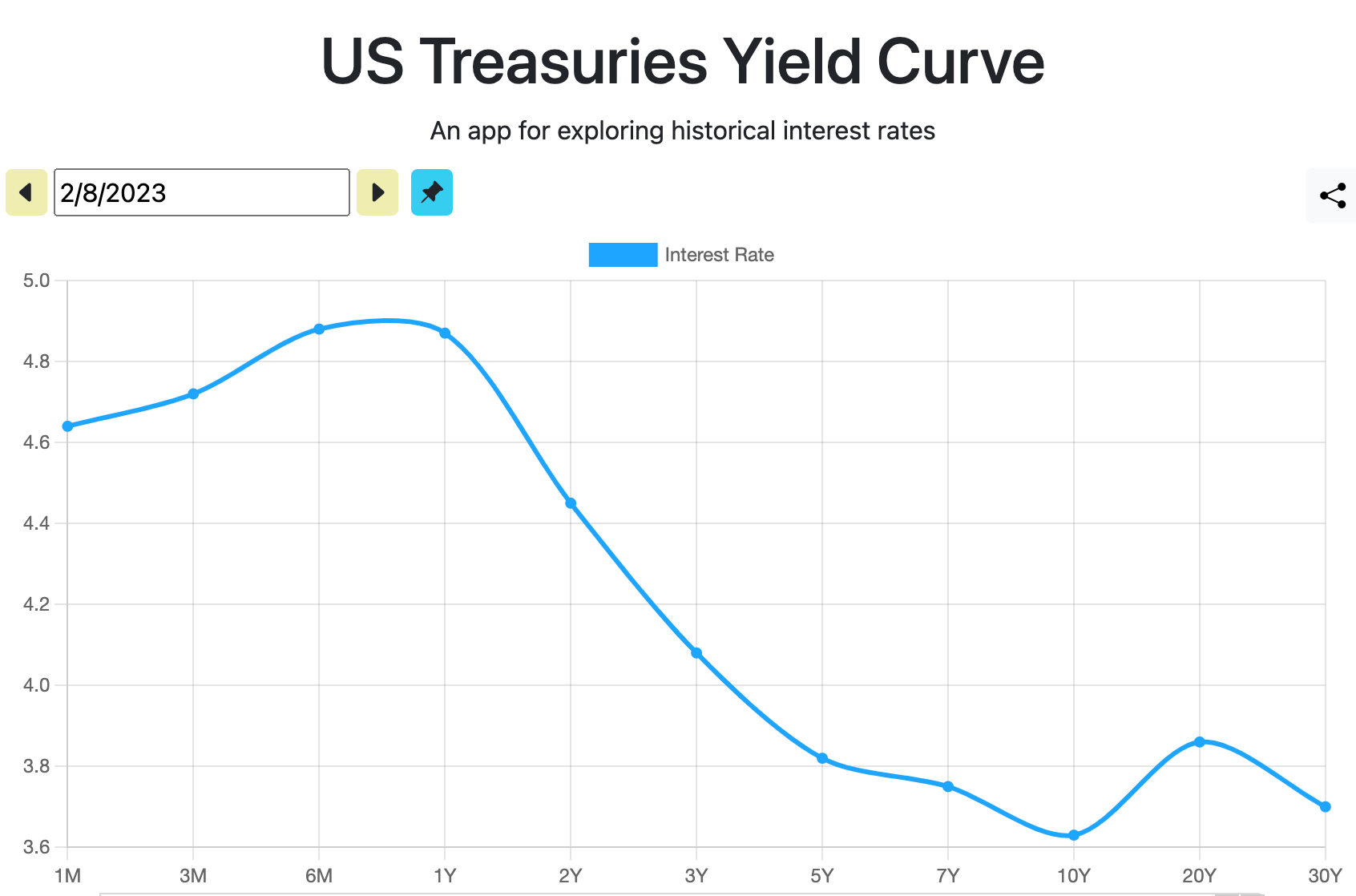

What we do know, however, is that with an inverted yield curve short-term interest rates are looking very attractive. Interest rates on 4-week and 8-week treasury bills are hovering above 4.5% annualized. That means you can earn north of 4.5% annualized on your cash, guaranteed, if you buy short-term treasury securities.

If you are sitting on cash and not sure what to do with it, this is a very good investment option to consider. These short-term “guaranteed return” investments effectively buy you time to see how the economic environment unfolds. I have personally put a portion of my investments in 4-week T-bills for now. If, after a month, I’m still unsure of the economic outlook, I’ll reinvest in more 4-week T-bills. Buy yourself some time. Buy U.S. treasury bills.

What are Treasury Securities?

Treasury securities are considered the safest investment out there as they are backed by Uncle Sam, the U.S. government. It is considered a risk-free investment as the U.S. government has never (and is not expected to ever) defaulted on its debt. With the U.S. hitting its debt ceiling there has been some controversy recently around whether the government will default on its debt. I wouldn’t worry too much about that. The U.S. has raised the debt ceiling every time it has hit it in the past.

Treasury securities are essentially how the government borrows money to fund its operations. The government "issues debt" by selling Treasury marketable securities such as Treasury bills, notes, bonds and Treasury inflation-protected securities (TIPS) to other federal government agencies, individuals, businesses, state and local governments, as well as people, businesses and governments from other countries. By buying treasury securities you are effectively lending money to the U.S. government.

Note: You do not have to be a U.S. citizen or be residing in the U.S. to purchase treasury securities.

Types of Treasury Securities

There are 3 types of treasury securities that differ based on length of maturity (you can learn more about treasury securities at the TreasuryDirect website):

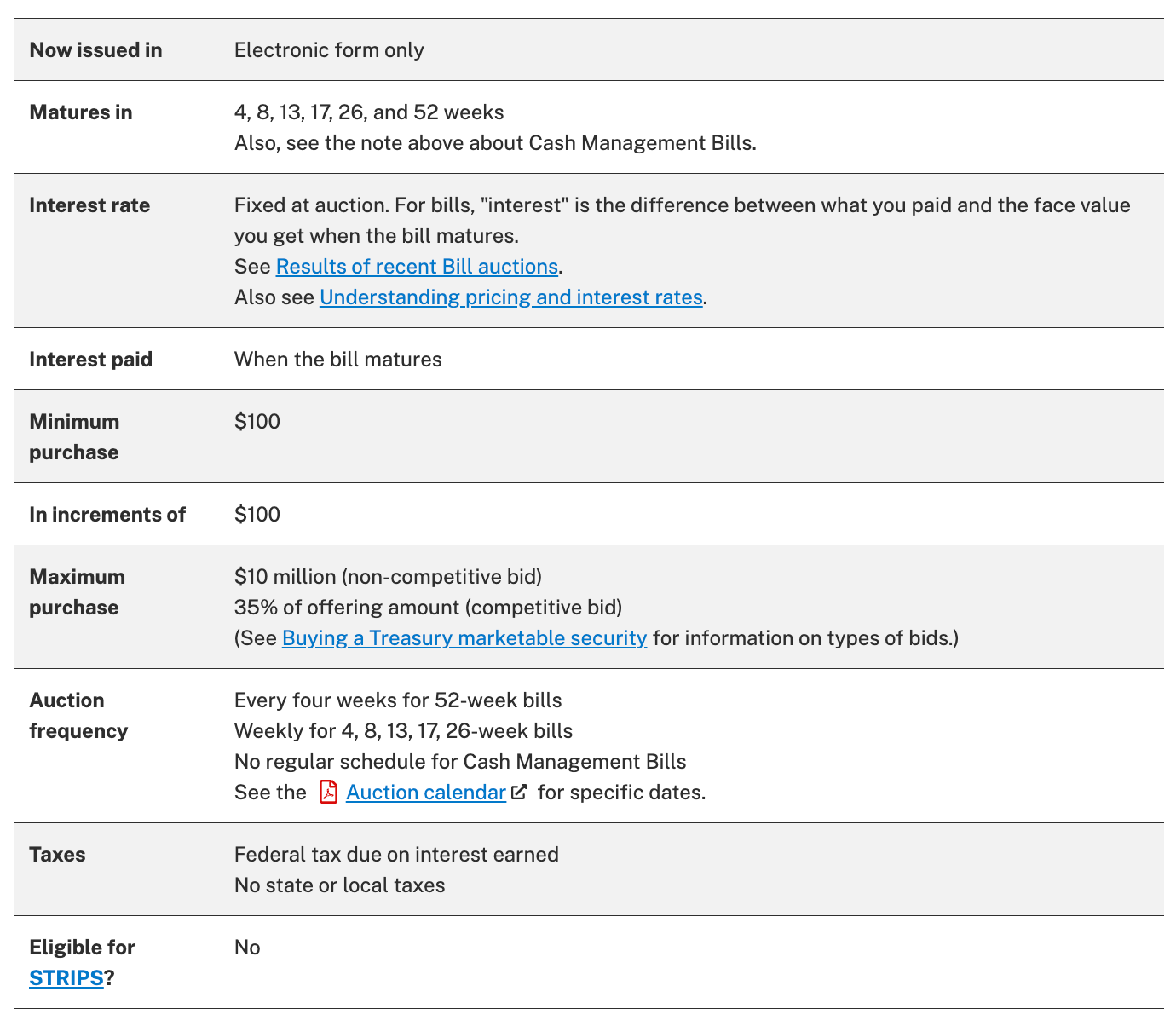

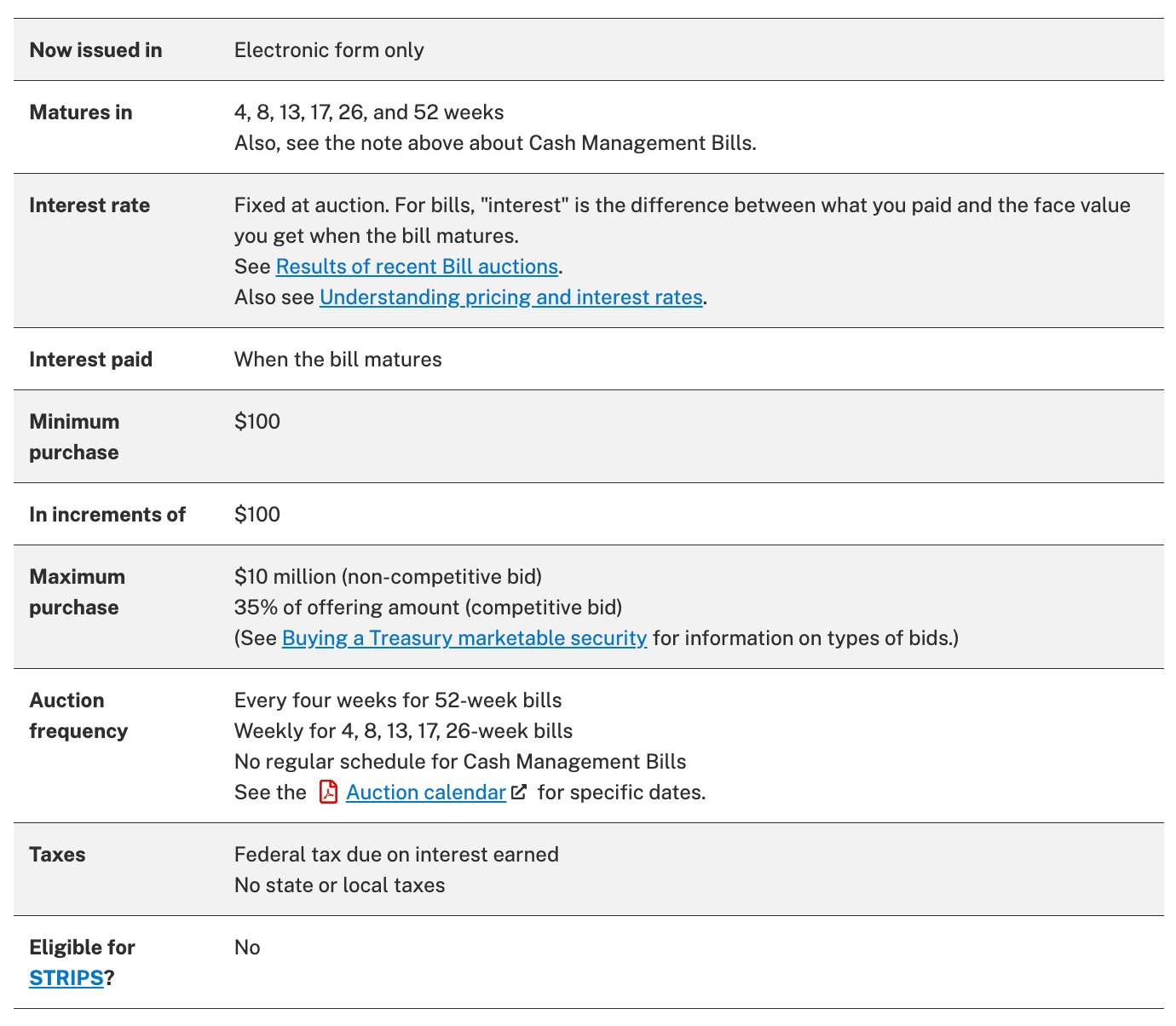

Short-term

5 term options: 4-week, 8-week, 17-week, 26-week, and 52-week

T-Bills are issued at a discount and mature at par value, with the difference between the purchase and sale prices constituting the interest paid on the bill

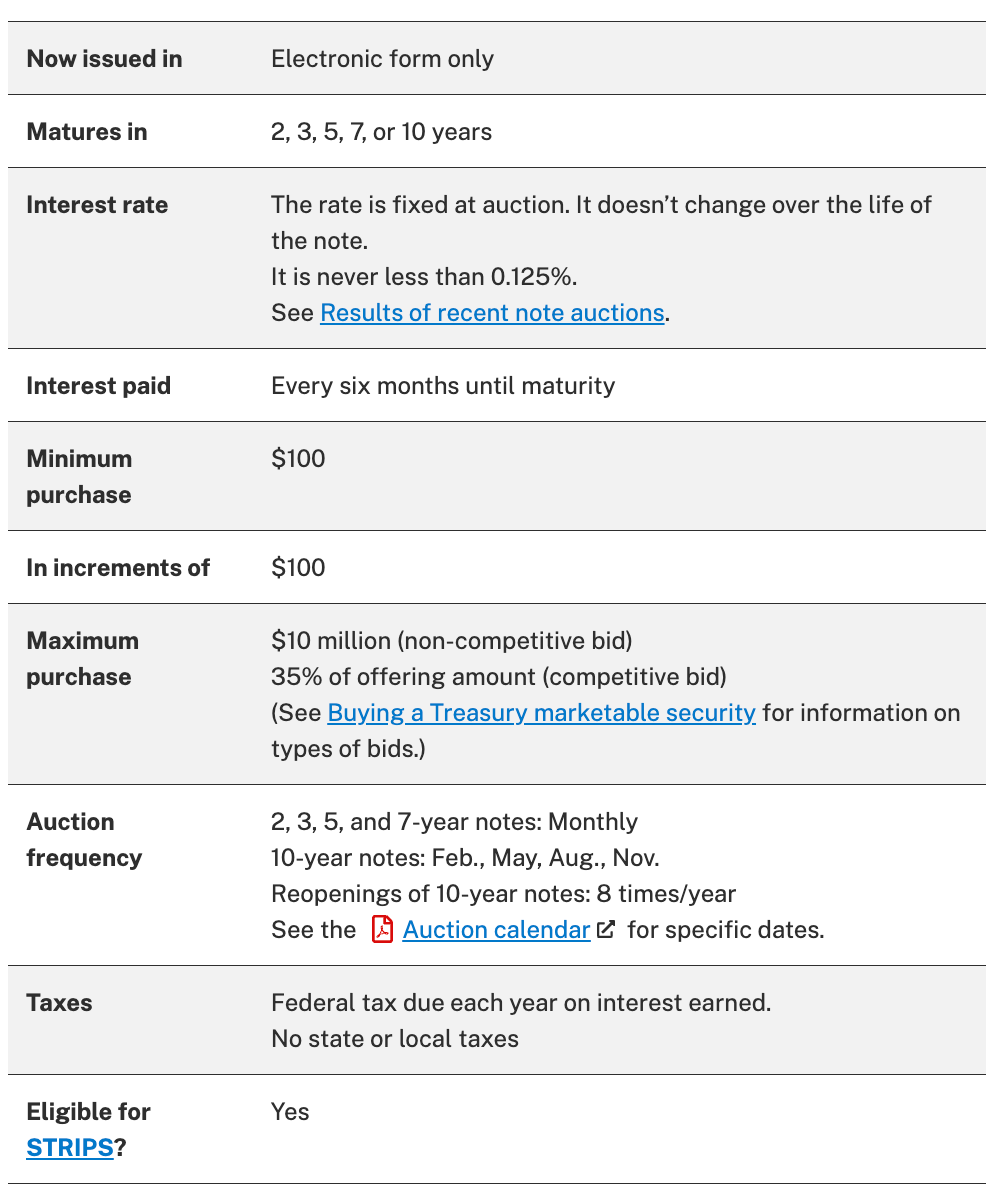

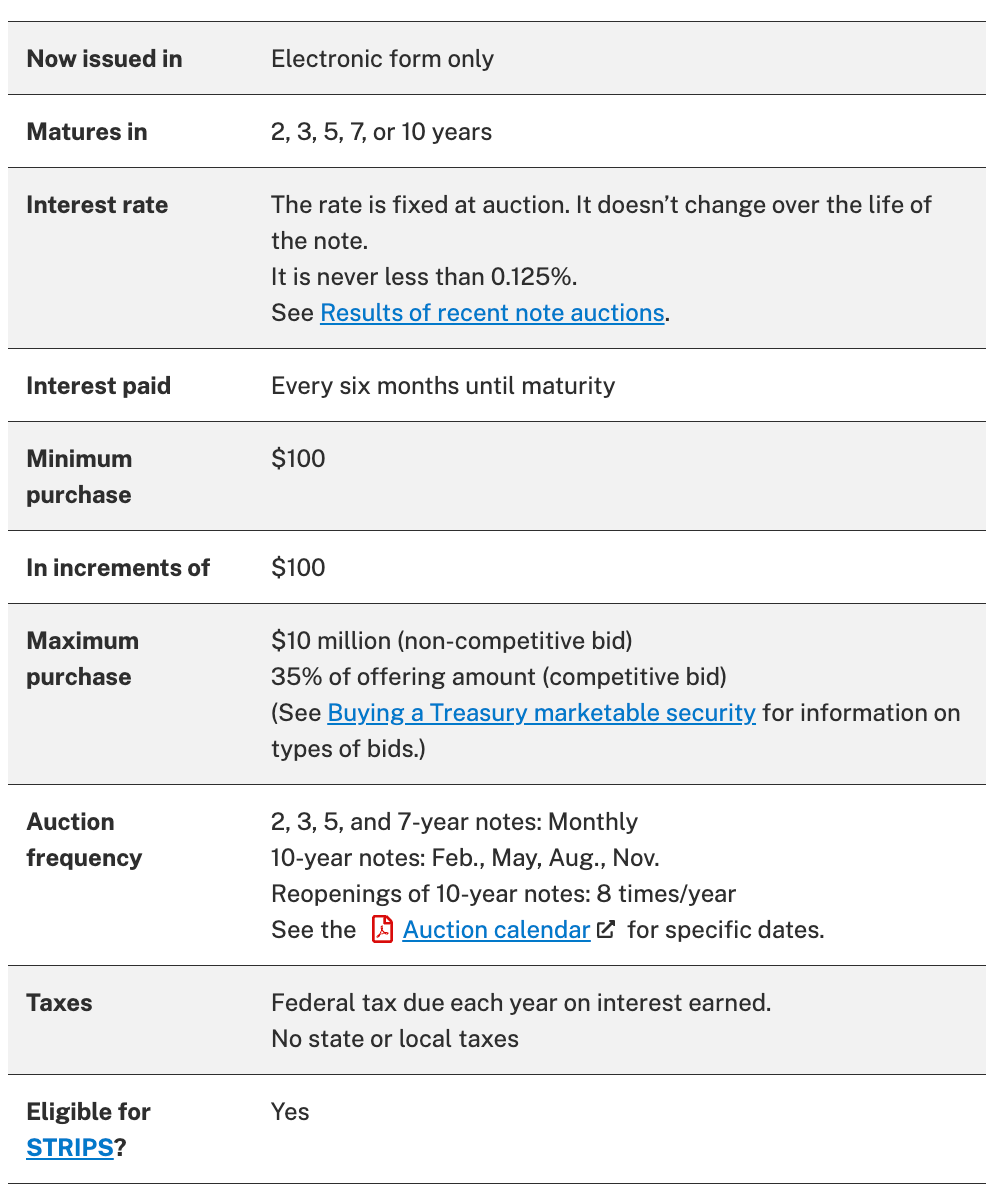

Medium-term

5 term options: 2 year, 3 year, 5 year, 7 year and 10 year

Interest paid semiannually

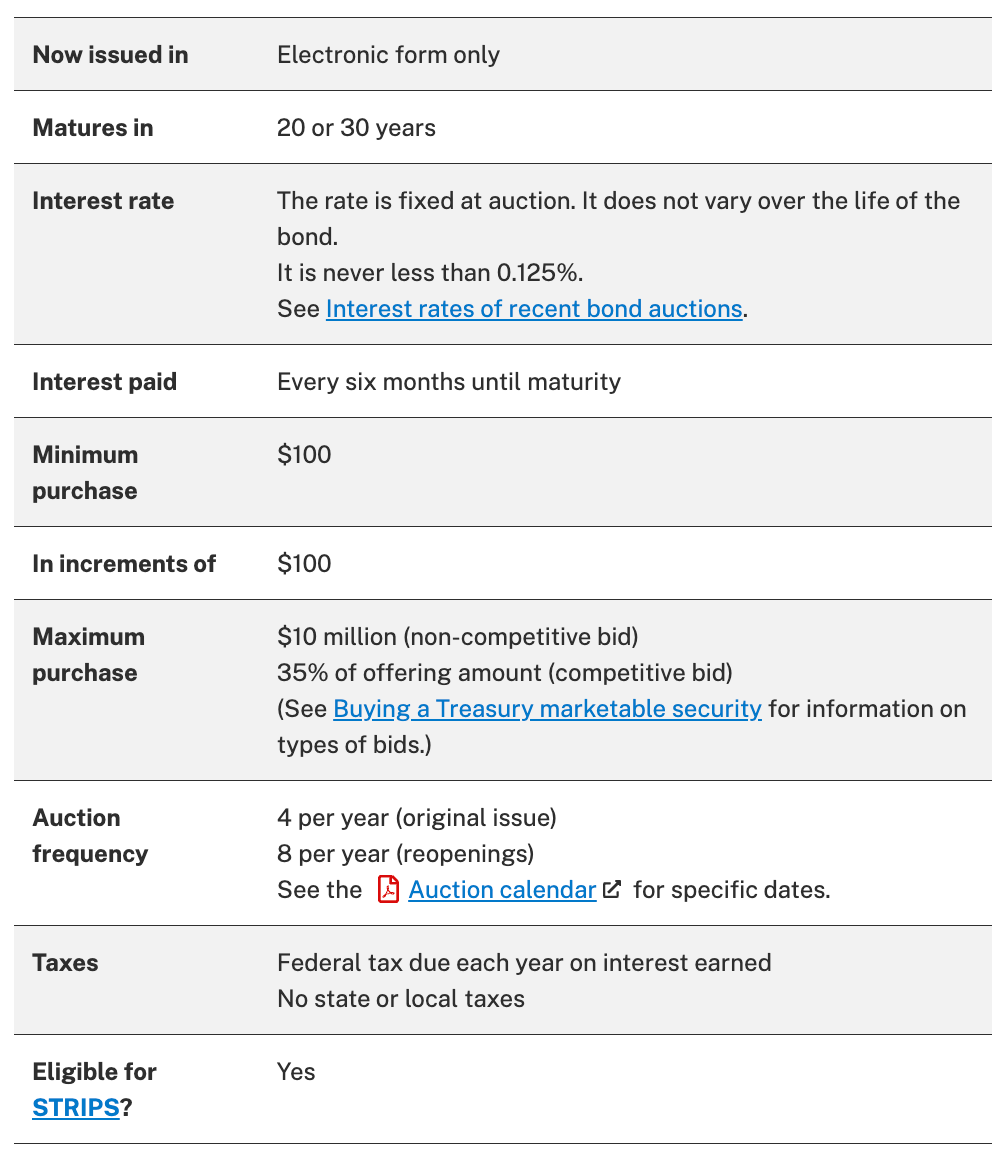

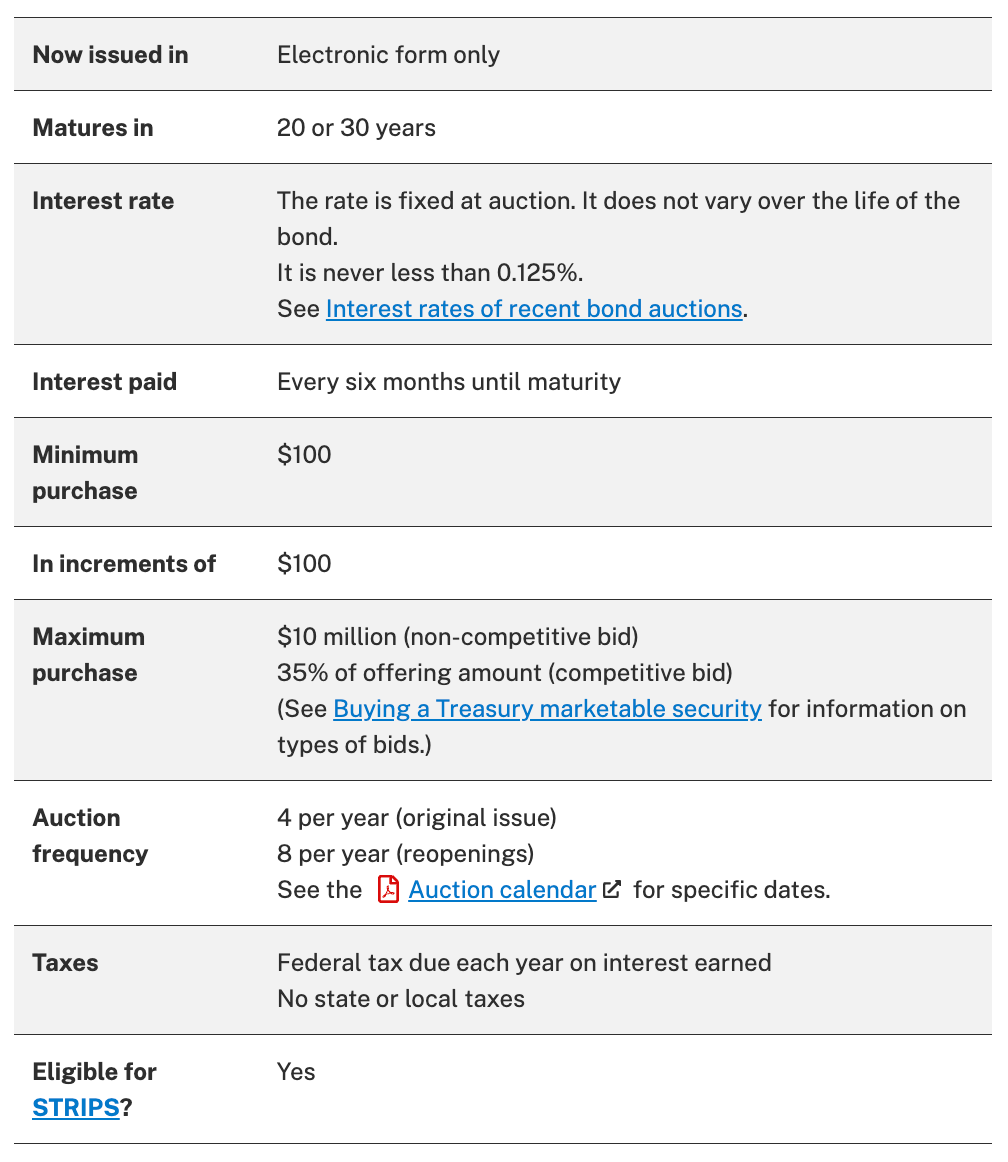

Long-term bonds

2 term options: 20 or 30 years

Interest paid semiannually

How to buy Treasury Securities

You can purchase treasury securities directly from the U.S. treasury at the TreasuryDirect website by creating an account and following their steps. Alternatively, your bank or brokerage account might also sell treasury securities at no fee. I personally use my primary brokerage, TD Ameritrade, as they don’t charge any fees. I believe Charles Schwab doesn’t either.

Auction process

First thing to know when buying treasury bills (or any treasury securities) is that they are sold through an auction on predetermined dates. Here is the link to the current tentative auction schedule pictured below:

There are 3 dates you need to be aware of:

Announcement date is the date the treasury security is open for purchase orders to be placed (you can place your purchase order till 8:30am ET on the auction date)

Auction date is the date the auction takes place. You will receive notice of your purchase price at the end of the auction date.

Settlement date is the date the transaction takes place.

Example: Let’s take the 4-week T-bill with a February 7 announcement date in the above picture as an example:

You can place an order to purchase this T-bill starting February 7 till 8:30am on February 9

The auction will take place on February 9 and you will be notified of your purchase price at the end of the day

Now that your order is locked in the transaction will take place on February 14, a week after announcement

The T-bill will mature in 4-weeks on March 14

Par value and the purchase price

The par value of treasury bills is $1,000 and the minimum purchase amount is 1 t-bill. So your minimum investment is close to $1,000. I say “close to” because when you purchase a T-bill the actual purchase price is a little less than $1,000. The difference represents the interest that you will earn on the security.

It is also important to note that you will not know the amount you are going to pay for the T-bill until the auction is complete because the auction actually determines the price. All you know at the time of placing your order is that the price you pay will be less than the $1,000 par value.

For example, let’s say you purchase 1 4-week T-bill and your purchase price after the auction ends up being $996. That means you will earn $4 in interest over 4 weeks, or a 4.8% annualized return.

Note: Interest earned on treasury securities is taxable at the Federal level.

If buying T-bills aren’t your jam, consider a high-yield savings account

If you’re banking with some of the larger banks like Chase or Bank of America you would have noticed that the rates on their savings account have not changed from that 0.01% they have been offering for more than a decade now. Smaller banks, on the other hand, are offering much higher interest rates. What gives?

Banks don’t actually have to increase the interest rates they pay on savings accounts in line with the Fed’s rate hikes. So large banks, flushed with customer deposits from a large customer base, don’t really need to increase their interest rates. Smaller banks on the other hand, are looking to grow their customer base, so they are increasing interest rates on their savings accounts to attract customers.

If you don’t want to buy treasury bills consider opening an account with a small bank with high interest on savings accounts. Some banks are paying more than 4%. Here is a list of banks with high-yield savings accounts to consider.

Thanks for reading!

If you enjoy this post please like ❤️ , subscribe 🔔 and/or share!

For short-form content check out my twitter, linkedin and instagram.

If you’d like to give me feedback or just shoot the shit, DM me on twitter.