4 alternative assets you can invest in today

4 alternative assets you can invest in today

Changing the game

Hey friends 👋

Time for #3 of the Wealth (W) series. Took a little longer than expected, but here we are! January was a month of research. I’ve been in a rabbit hole exploring alternative investment options and having a blast doing it. There is an entire world out there outside of equities just waiting to be explored. My curiosity alarms are ringing. My explorer hat is on. Too early to say whether my excitement is driven by the sheer novelty or true interest, but feels like the later. January has also been a month of experimentation. I’ve been playing with posting short-form content on Twitter, Linkedin and Instagram to quickly summarize my research. Today’s newsletter is, in a way, an aggregation of that research. It’s also the start of a deeper dive into alternative investment asset classes.

Public markets have served as the gateway into the realm of investing for most retail investors throughout history. With near-zero interest rates until recently, fixed income instruments like bonds were not attractive. Equity markets served as that gateway for investing newbies. Thanks to advancements in technology and companies like Robinhood, investing in stocks has become very simple. Borderline game-like. The market is easily accessible and extremely liquid. Stocks are like the “pop” music or “top 40” of investing. Mainstream, overplayed, but still loved and talked about by everyone.

Everyone was a trader in 2021 and everyone was a loser in 2022. Tech, our golden goose, plummeted. Nasdaq ⬇️ 33.1%, S&P 500 ⬇️ 19.4% and Dow Jones ⬇️ 8.8%. Even bonds, our famed stock “balancer”, fell.

2022 was humbling to say the least. A lesson in greed, economics, bubbles, inflation, interest rates, supply chain, war, Jerome Powell, eggs… all at once! 😅 It became clear that relying solely on the stock market for returns was not a viable option. With high inflation and increasing interest rates the fundamentals of the market have changed, and might remain changed for a while. So what should a return-hungry retail investor do? It was time to expand my taste beyond “top 40”.

If you can’t beat the odds, change the game. The game is no longer just stocks. It’s building a diversified portfolio of investments with multiple asset classes. Does that mean I’m going to stop investing in stocks? Hell no. The degenerate in me will still look for that stock that has the potential to be a multi-bagger. I enjoy investing in stocks. I enjoy conducting due diligence. I also enjoy the rush. It’s exhilarating, adrenaline inducing and exciting. Spoken like a true gambler… yes, I know. I’m not trying to hide it.

That being said, my pool of “risky” stocks (yes, investing in individual stocks is risky) will, going forward, be a very small percentage of my portfolio. With a volatile market in the short-term, I am not looking to invest in stocks anytime soon unless I come across a real opportunity.

Stocks have always been fun to invest in ESPECIALLY in a growth-favored environment, like the one we saw between 2008 and 2021. Earnings beat + positive outlook? Stock price 🚀. No brainer. You could pick your favorite company, look at their fundamentals, run your analysis, and voila… you have an investment thesis. We didn’t really have to care much about the macro economy.

Tech met that need. Growth represents endless opportunity and tech exemplified nothing but that. Take risks, grow fast (or fail fast), do first & ask for permission later, innovate, test crazy products. Show me the growth numbers. Users? Primary. Revenue? Secondary. Profit? Nowhere in sight. Can the business sustain itself without raising capital? No, but why would you want to prioritize that over growth anyway? It worked really well. Too well. Now looking back it’s pretty evident that it worked so well because capital was cheap. Interest rates were zero. Hell, they were technically less than zero with quantitative easing. Growth was favored. We were effectively being paid to spend money. How utopic.

We’re in a different macroeconomic environment today. Inflation and interest rates are high. Growth is now the enemy. We flooded the economy with cash. We grew too fast. Prices are catching up. We aren’t ready. We didn’t realize the consequences. The Fed, however, did (or should have?). It’s shocking to me that the top economists saw inflation as “transient” after doubling their balance sheet, but that’s a rant for another time. Fact is the Fed wants to slow the economy down. Shrink its inflated balance sheet. Reduce money supply. Hit the breaks. Get this behemoth-of-a-ship back on course. In 2020 we turned this cruise ship into a speed boat and now the breaks aren’t working as effectively.

The future is uncertain. We could go into a recession this year or we could narrowly escape. There are enough arguments for either scenario to play out. If we escape the recession, the S&P 500 could end the year higher. Looking at history, back-to-back down stock market years have been rare. The S&P 500 has had two or more consecutive negative years of return only 4 times since 1928: 1929-1932 (great depression), 1939-1941 (World War II), 1973-1974 (oil crisis) and 2000-2002 (Afghanistan/Iraq post 9-11). Will this be the fifth time in a century?

The facts remain:

Inflation is still high even though its slowing meaning:

In the short-term, prices will continue to rise although at a slower pace than we saw in 2022

In the long-run, high(er) prices are here to stay

Interest rate hikes are slowing (may even stop), but:

They will remain high in the short-term

Even if the Fed starts cutting interest rates at some point, they will not go down significantly

Where should you look for returns? It’s no secret that investing in stocks is fun because of the potential for outsized returns, the dopamine hit you get from making the right call. The fun is in the action, the risk, the uncertainty. It’s why we enjoy picking stocks even when we are well aware that it’s very hard to beat the market. Most mutual funds don’t. What makes you think you’re the genius that’s going to. And even if you do, on occasion, in the long-run the market is going to win. Investing in the S&P 500 month-after-month over a long time horizon will net you the best annual returns. But, it’s boring.

So how do you invest AND have fun? One way is through alternative investments. Instead of relying on the dopamine hit from a trade for the “fun” in investing, invest in something fun, like wine 🍷 or art 🎨. It’s a great substitute - surprisingly good returns, a lot to learn for a true hobbyist, great dinner/date conversation, and most importantly, a great way to diversify your portfolio in times of uncertainty. You no longer need to rely on Dos Equis to be the most interesting man (or woman) in the world.

What are alternative investments?

Alternative investments are asset classes that aren’t stocks, bonds, or cash. They tend to be private investments although aren’t exclusively. They differ from traditional investment types because they typically are not easily accessible, require sizable capital, require niche expertise, are illiquid, and most importantly, have a low correlation to traditional equities.

Here are 7 broad categories of alternative investments:

Private equity / debt

Venture capital

Hedge funds

Real estate (e.g., farmland, timberland, commercial, residential, etc.)

Commodities (e.g., agricultural products, oil, natural gas, and precious and industrial metals)

Collectibles (e.g., fine wine, art, vintage cars, stamps, coins, etc.)

Crypto

Note: I will not be focusing on crypto because of all the hype around it.

Alternative assets have historically only been available to institutional investors or high net worth individuals because of the large minimum investment requirements. Tech, however, is changing the game. Not only have we made stock market trading more accessible, developed robo-advisors, enabled open banking, and created banking-as-a-service, we have also built platforms that make alternative investments more accessible (W1: New Wealth, Who Dis? focuses on the tech journey to today that has made these innovations possible). No longer do you have to have a large amount of capital and expertise to invest in alternatives. Expertise is packaged into the platforms’ service and the minimum capital requirement has reduced tenfold by increasing the investor pool.

4 attractive alt investments

The world of alts is expanding rapidly and access to them is getting easier as more platforms emerge. In addition to investing in real estate, VCs and startups, you can now also invest in fine wine, art, sports cards, sneakers, whiskey, music and more.

The way I see it, adding alt investments to a portfolio smoothens out long run returns. I haven’t run the math (yet), but looking at historical returns of alts like farmland, fine wine and art, it’s clear that including them in a portfolio will reduce the standard deviation of your portfolio returns (that’s stats jargon for less extreme returns both on the -ve & +ve sides).

Will I have outsized returns every (or any) year? No. Can I average >10% annually over a long time horizon? Likely. I envision the portfolio to include:

S&P 500 index (the benchmark that provides ~9% annual return over the long run that every fund manager tires to beat)

Alternative assets (provides diversification to the S&P index, serves as an inflation hedge, and lets face it… is really really fun)

Specific stocks (solely to satisfy my degenerate, risk-taking, rush-chasing nature)

Fixed income like bonds (the most boring part of the portfolio. the necessary evil, the ying to the equity yang, because they provide stable returns, albeit boring, returns)

The composition of the portfolio would depend on the macro environment. I have a lot more work to do to study historical returns of a combined portfolio of these assets with different weights. Lots more experimentation. Lots more to learn. A lot more fun up ahead. I will publish a newsletter on what portfolio compositions look attractive once I’ve run the numbers.

Getting back to the meat of today’s newsletter, let’s dive into some attractive alt investment options. As much as I would have loved to spend time doing soup-to-nuts due diligence on each alt investment, it wasn’t the most logical place to start given the breadth of alt investment options to choose from. The reality is, each alt investment is niche and requires its own set of expertise, which takes time to develop. More time than you think. It’s why alts aren’t an easy investment decision. Most investment professionals in the space have years of experience and focus on one specific alt. Its not as simple as comparing companies that use accounting principles to put together financial statements that can be compared like-for-like across companies. The metrics and “language” are different. In the wine market, for example, there are wine scores that are determined by wine advocates like Robert Parker that drive the price and popularity of a vintage of wine.

Lucky for you and me, there now are alt investment platforms that cover everything from raising capital to sourcing deals to due diligence to closing. Without any expertise they are the best options to scratch my initial curiosity itch. Here are 4 attractive alternative investment asset classes that you can invest in today with relatively low min investment using online platforms:

Farmland 🚜

Fine Wine 🍷

Art 🎨.

Real Estate 🏠

Farmland 🚜

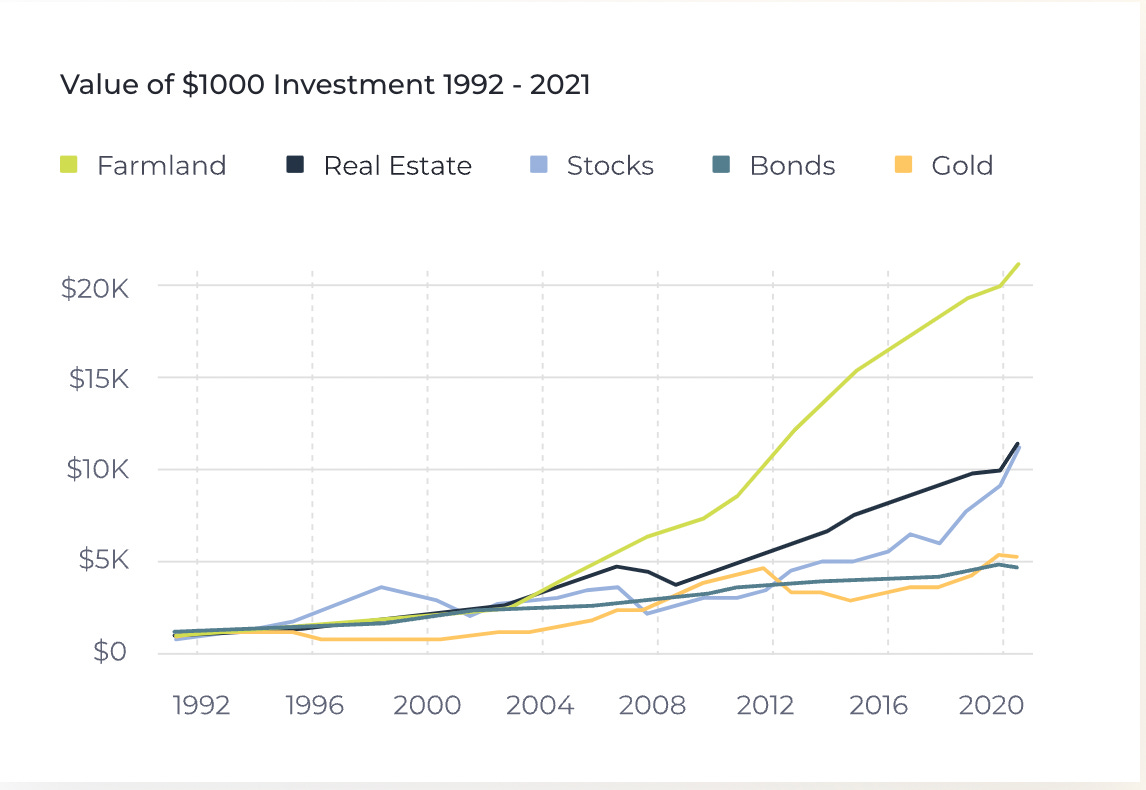

Farmland had an amazing year in 2022 returning 10.21% in 2022 proving to be a good hedge against inflation.

What is Farmland 🚜?

Farmland is land that is specifically used for growing crops or raising livestock and that has been allocated in zoning laws for agricultural purposes.

Farmland depends on 2 sources for return:

Land appreciation

Net cash flow from produce

High annualized historical returns

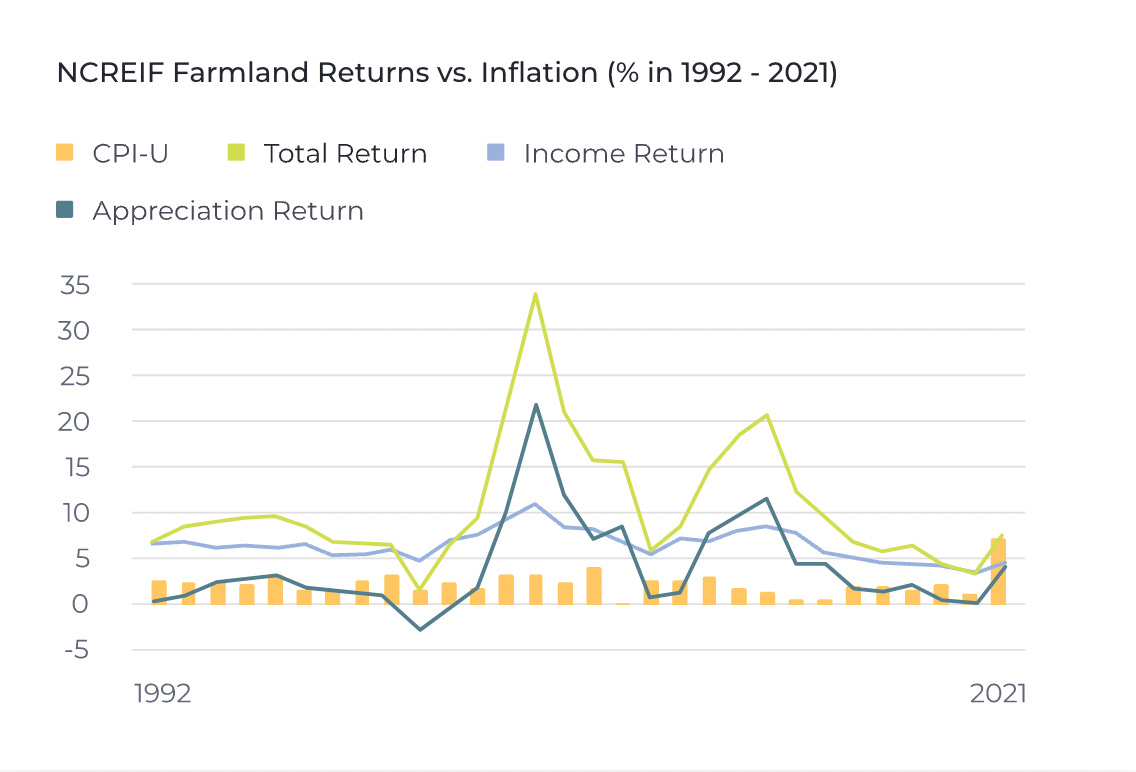

The most comprehensive benchmark for Farmland returns is the NCREIF farmland index.

Since 1991, US farmland has returned 10.7% annualized including both income and appreciation.

Low volatility

Farmland 🚜 has experienced historically less volatility than both traditional and alternative asset classes, and has provided stability for investors during market downturns.

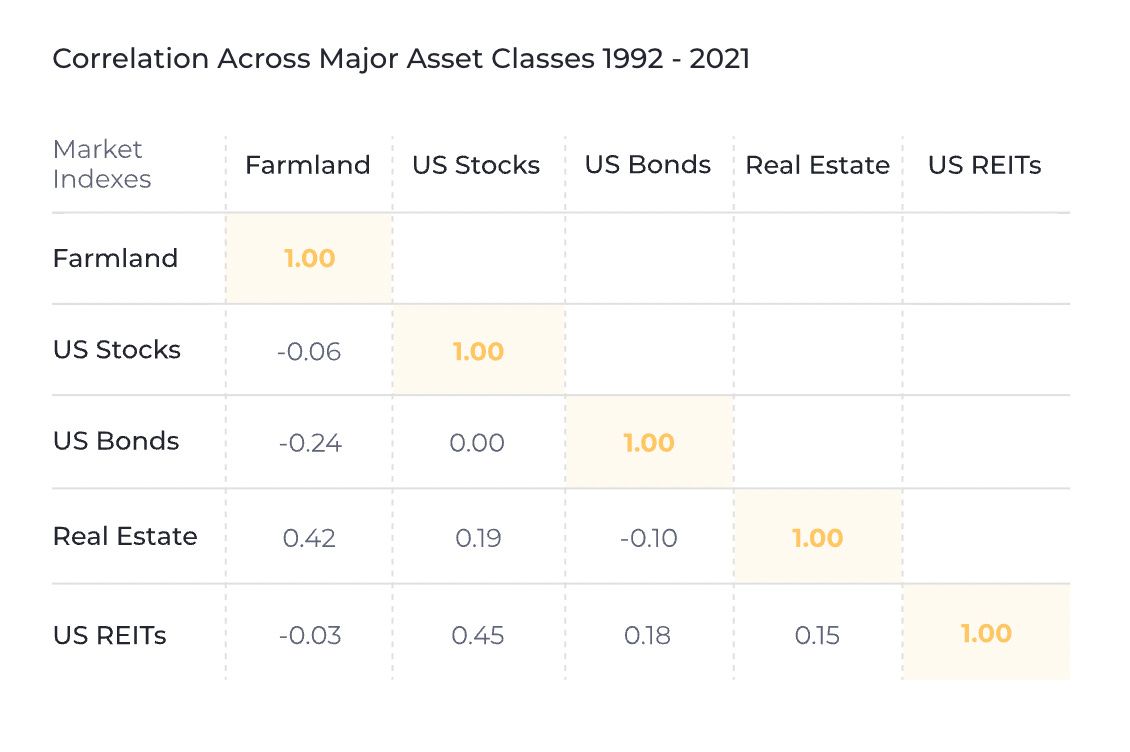

Great diversification play

Farmland 🚜 returns have been historically uncorrelated to conventional assets, such as stocks, bonds, and real estate, and broader market indices.

Inflation hedge

Farmland has historically been one of the best inflation hedges

Even with rising inflation, Farmland 🚜 returned 10.21% in 2022

In the midwest, Farmland jumped a whopping 20% in Q3 alone from a year earlier

Three reasons why Farmland increased so much in value in 2022?

Higher revenue from increase in commodity prices

Higher demand with pandemic-induced population shifts

Higher demand for renewables like diesel

How to invest in Farmland?

REITs ($FPI & $LAND) - easiest option, but not the best exposure

Purchase farmland - takes effort to acquire, manage and dispose

Own shares in Hedge Finds with farmland exposure - requires large capital base

Alternatively, use farmland crowdfunding platforms:

FarmTogether is an online marketplace for farmland investing. It provides accredited investors with direct access to pre-vetted U.S. farmland investment opportunities. Investors can invest directly in specific farms or in a fund that holds several farm investments.

AcreTrader is a crowdfunding platform that provides accredited investors with direct access to farmland. Most of its offerings require an investor to buy 10 shares, which is equivalent to one acre of land that generally costs between $3,000 and $10,000 per acre. Instead of holding the legal title to the physical acre of land, investors own shares in a limited liability corporation (LLC) that holds legal title.

FarmFundr is a crowdfunding platform that allows accredited investors to invest in a variety of opportunities like farmland and agricultural facilities.

Farmland LP focuses on buying commodity farmland and converting it into more valuable organic farmland. It offers accredited investors the opportunity to participate in a private equity fund that has the flexibility of eventually becoming a REIT and going public.

Harvest Returns is a crowdfunding platform offering a variety of agricultural deals that are mainly open to accredited investors.

All except Harvest Returns, require investor accreditation

Notable Farmland investors

Bill Gates is the largest private owner of farmland in the US owning 275k acres (0.3%)

Warren Buffett has owned a profitable farm for more than three decades raving about how the farm has tripled its earnings and is worth five times after 28 yrs

Things to know before investing in Farmland

Rising rates & a potential recession could hit Farmland

Farmland was flat from 2014 to 2020 during the commodities bear market

Investment is locked-in for a long time

Fine Wine 🍷

High annualized historical returns

Fine Wine returned 10.6% per yr over the last 30 yrs

That’s slightly higher than the S&P 500, which delivered 9.09% per yr over 30 yrs

Recession resistant

A lesson from 2022 - when inflation and interest rates are rising, previously uncorrelated asset classes start moving in the same direction… down ⬇️

Stocks, bonds and crypto fell in 2022

Fine wine however stood strong with a 20.54% gain in 2022

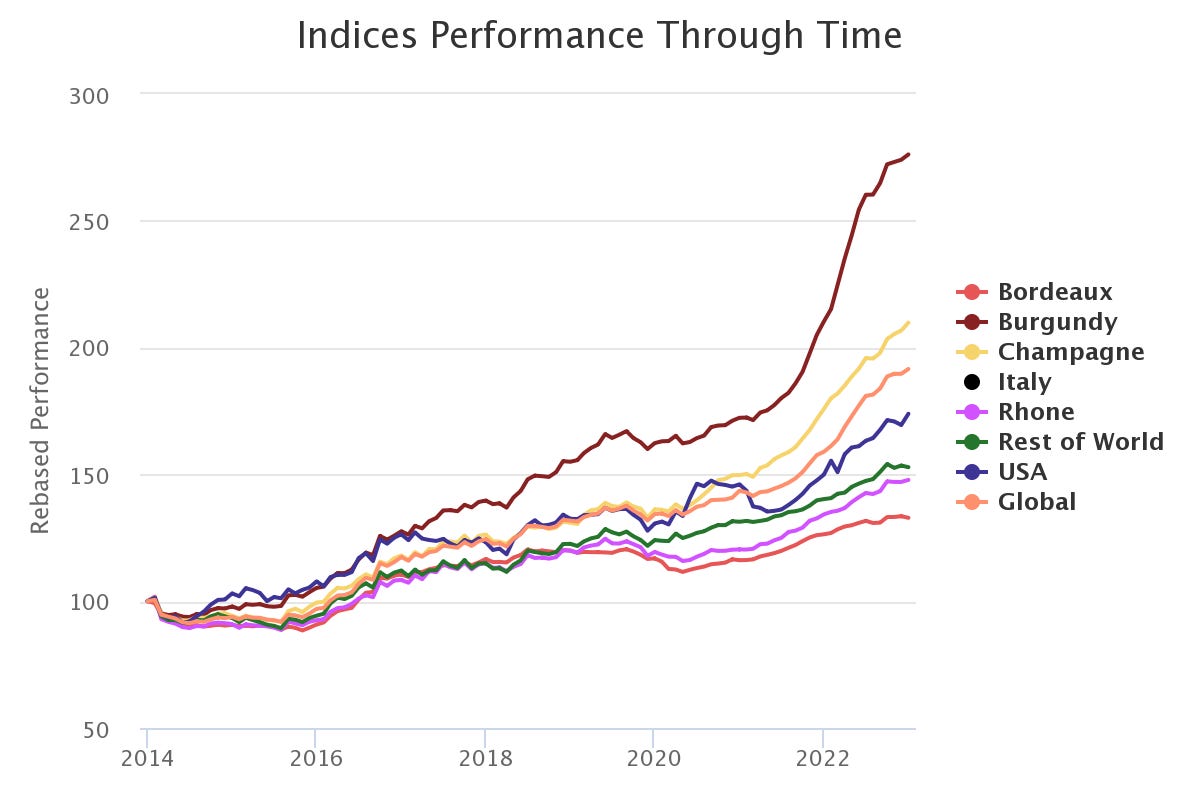

Not all fine wines are made equal

Burgundy and Champagne continue to lead the way over the past 7 years with majority of gains coming in 2022

Burgundy and Champagne gained 31.31% and 19.35%, respectively, in 2022

How to invest in fine wine

If you have the time and money to conduct due diligence you can:

Buy wine bottles

Buy a vineyard

Invest in wine stocks and companies

Alternatively, you can sign up for fine wine investing platforms like VinoVest and Cult Wines

VinoVest is a Series A, LA-based startup that allows you to invest in fine wine w as little as $1k for 2.5% in fees

They have 3 other plans:

Plus: $10k min for 2.35%

Premium: $50k min for 2.15%

Grand Cru: $50k min for 1.9%

Cult Wines is a UK-based company that allows you to invest in fine with w as little as £10k for 2.95% in fees

They have 3 other plans:

Premium Cru: £25k min for 2.75%

Grand Cru: £100k min for 2.5%

Cult Cru: £500k min for 2.25%

Here is Cult’s report on the performance of fine wine in 2022 and their indices

Art 🎨

We appreciate it for its beauty, creativity, feelings it invokes, the story... sometimes we don’t even know why

It’s hard to compare and its hard to value… making it a unique asset class

High annualized historical returns

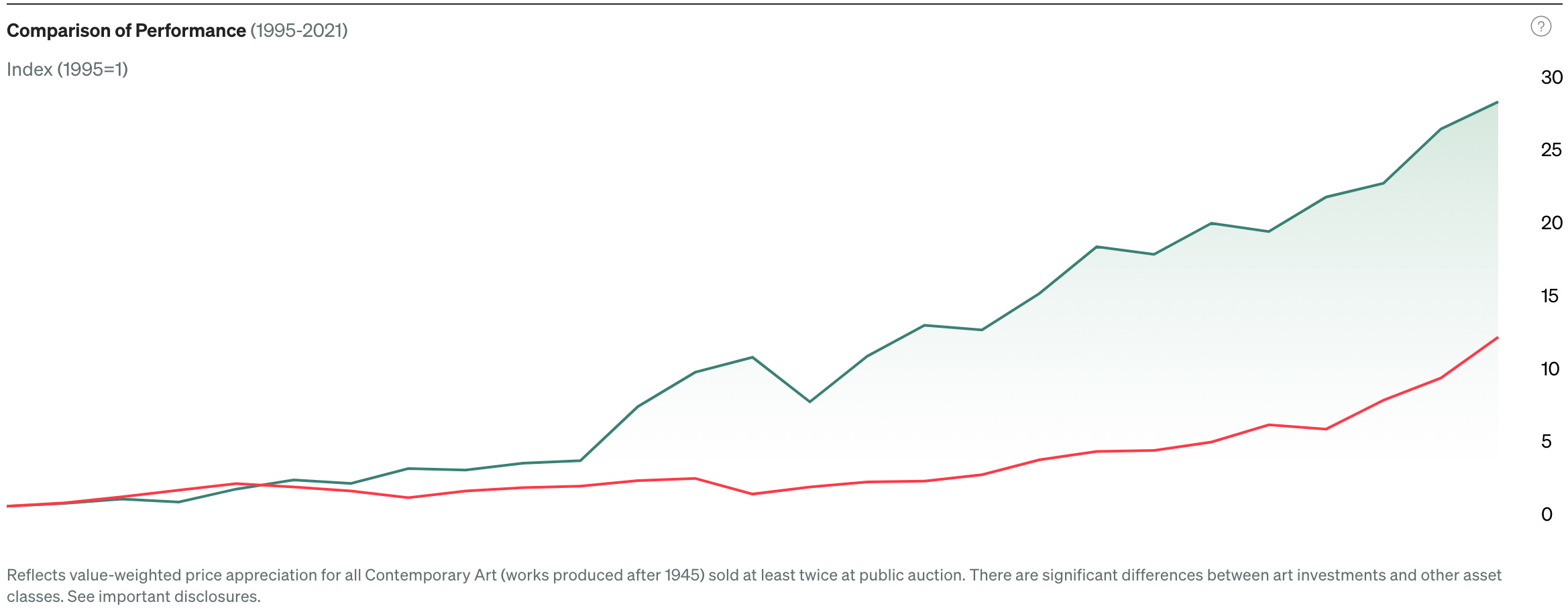

According to the Art Basel & UBS 2022 Global Art Market Report, global art sales surpassed $65.1B in 2021, up 29% from 2020

Contemporary art returned 13.8% annually between 1995 and 2021 compared to the S&P return of 10.2%

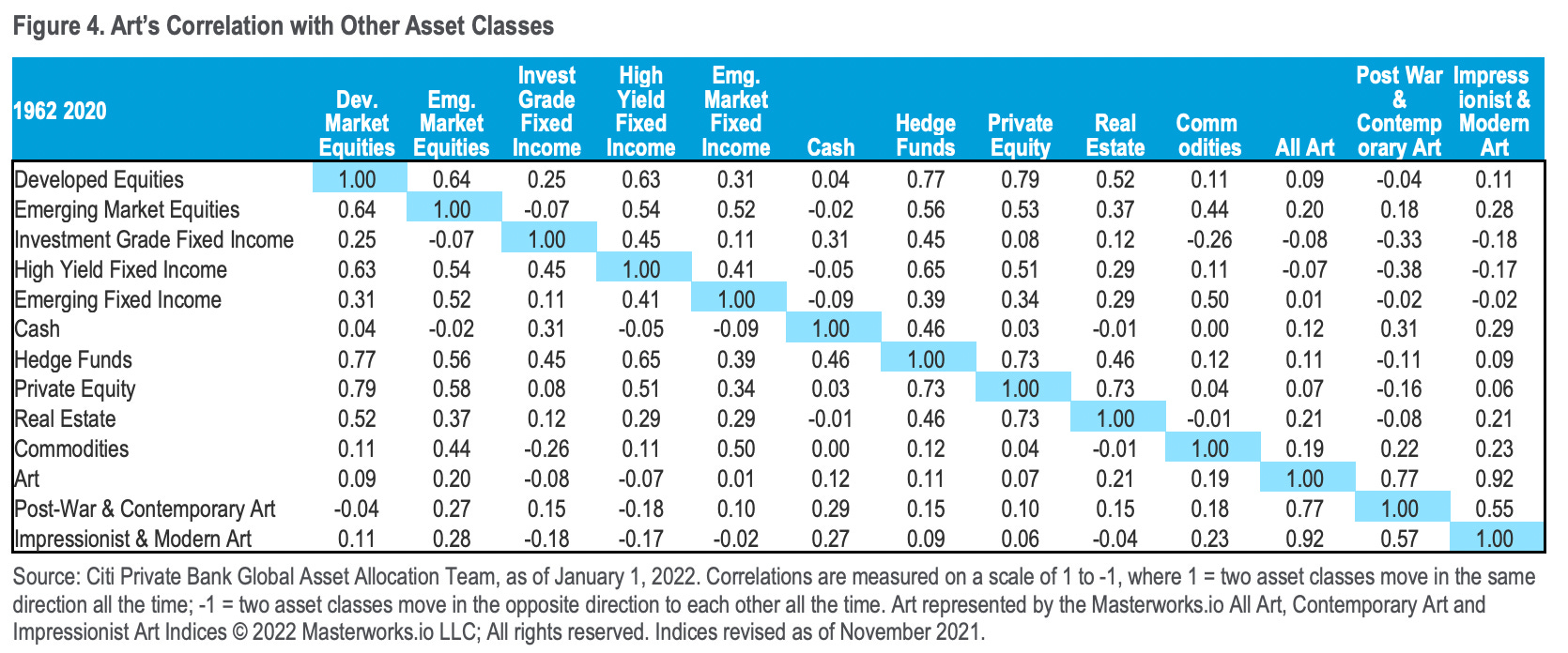

Low correlation to traditional markets

Citi’s Private Bank published a report in March 2022 that highlighted a low correlation between art and all other asset classes, making it a good diversification play

Inflation hedge

From 1985-2020 when inflation was equal to or higher than 3.0%, Post-War & Contemporary art prices had an annual average real price appreciation of 23.2%

Aesthetic value that appreciates

Compared to other investment vehicles, art is an asset that you can enjoy while holding it in your portfolio

It’s where the bulk of its value comes from

Risks

Illiquid: Investment locked for a long time b/c art isn't easy to sell quickly

Expensive: Buying / maintaining (handling, storage & insurance) art comes at high costs

Counterfeits: Unless you are well informed its easy to get duped

Types of art

Old masters: Pristine art created by renowned, historically-significant painters; hard to acquire

Blue chip art: Art from established, sought after artists; reliable investments

Up-&-coming: Artists yet to reach popularity; highly speculative

How to invest in art

If you have the money & expertise, you can buy artwork at auctions, galleries or fairs

Otherwise, use fractional ownership platforms like Masterworks and Yieldstreet:

Low min investment

Due diligence, purchase, maintenance and sale taken care of

Masterworks analyzes, buys & stores art, then offers shares to each piece

After a holding period, Masterworks will sell the piece & distribute any profits

Art is insured and transactions are regulated by the SEC

$10k min investment; 1.5% management fee; 20% profit fee

Yieldstreet gives access to portfolios of art-backed loans & pools of fractionalized shares

They lend your money to a co that wants to make an art fund; you get regular P&I payments on the loan

SEC regulated co and debt is insured

$10k min investment; 1-4% management fee

Residential Real Estate 🏠

Real estate, the largest asset class in the world valued at ~$280T globally, has been the OG alt investment for decades. It’s not liquid, takes a lot of time and effort to manage, but has a lot of benefits if done right.

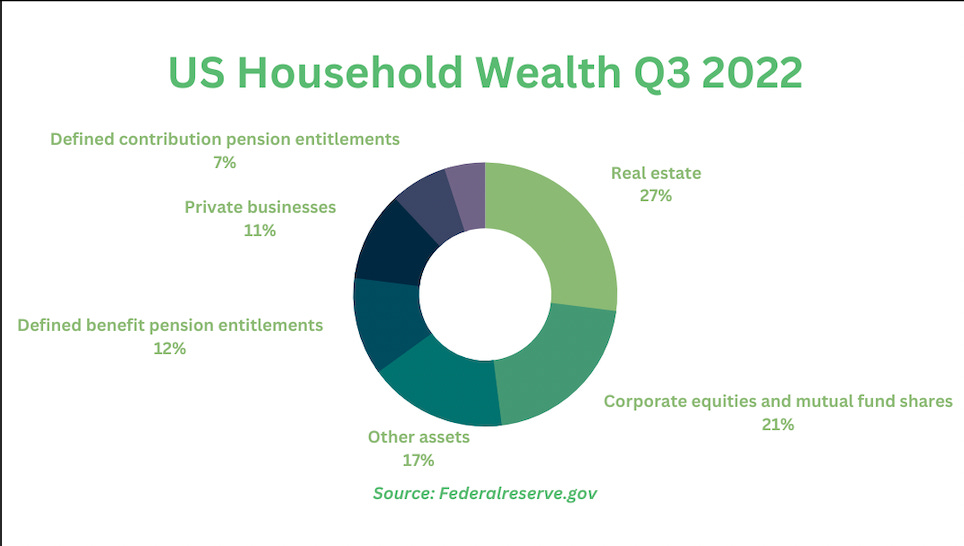

In the US, Real Estate accounts for 27% ($41.9T) of total household wealth, the largest category

Benefits

Attractive long-term returns

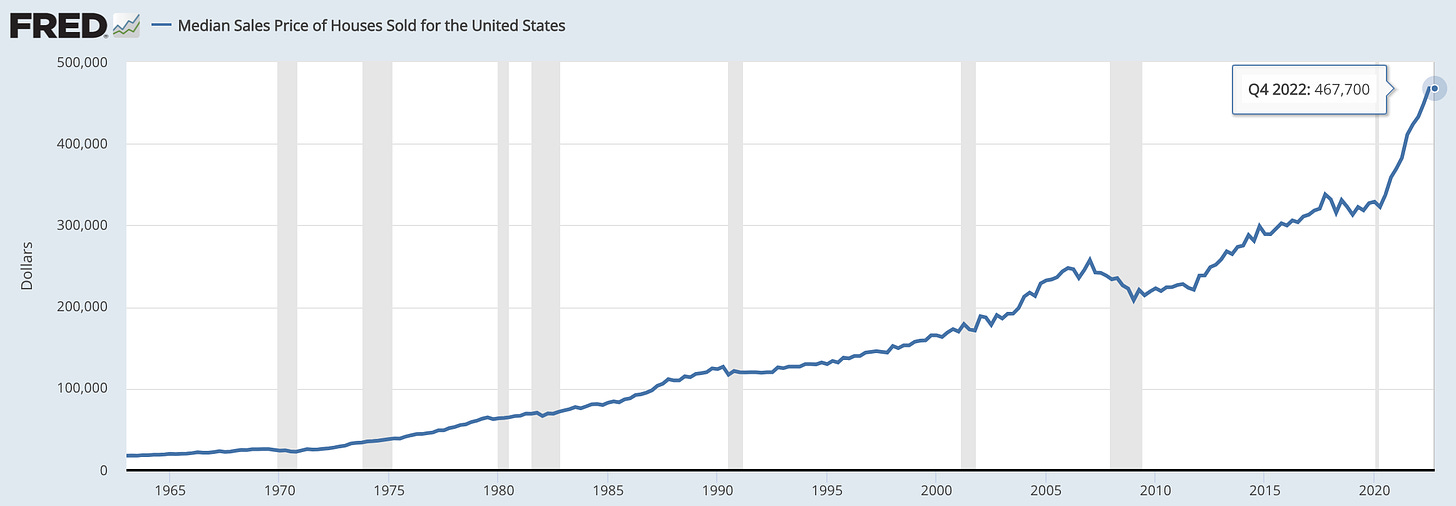

Median home sale prices in the US have increased ~9% annualized over the last 30 years, similar to the S&P 500’s return of 9.09%

Steady cash flow

You can rent out your property and earn monthly cash flow

Cash inflow can be guaranteed even if property appreciation is not

The goal is to be net cash flow positive (i.e., cash inflow > cash outflow of mortgage, maintenance, taxes, etc.)

Tax advantages

Write-off expenses tied to operation, management & maintenance

Depreciate property & improvements

Pay cap gains tax instead of income tax on sale of property

Pass through deduction of up to 20% of QBI on personal taxes

Defer taxes through 1031 exchange

Inflation hedge

Inflation started rapidly increasing after March 2021 and peaked in June 2022 at 9.1%

During this period

Median home sale prices in the US increased 17.4%

S&P 500 was down 4.7%

Downsides

Capital-intensive

Management-intensive

Illiquid

Due diligence requires time and effort

Liability risks (e.g., getting sued)

Risks

Market can be unpredictable

Choosing a bad location

Unexpected negative cash flows (vacancy, increased expenses)

Problem tenants

Hidden structural problems

Low liquidity

What’s happening in the real estate market today?

Home prices have started to fall

With rapidly rising interest rates, fewer people are looking to buy homes

At the same time homeowners are less likely to sell their properties as they have locked in low interest rates

According to a study conducted by Fortune, 24 of 29 leading housing market researchers predict that national home prices have further to fall

Some markets are predicted to fall more than others

Its not a good time to invest in real estate if your are looking for property appreciation, however, you may be able to find a few cash flow positive deals depending on the numbers

How to invest in Residential Real Estate

Buy rental property: capital intensive, requires time and effort

REITs: relatively more liquid, less effort, but can be more correlated to the stock market

Investing platforms: low capital requirement, less effort, more liquid

You can get started with as little as $10 on Fundrise

Other platforms to consider:

Note: some require accreditation

Disclaimer:

This is not investment advice

You should perform your own due diligence for any investment you make or consult a financial advisor

Thanks for reading!

If you enjoy this post please like ❤️ , subscribe 🔔 and/or share!

For short-form content check out my twitter, linkedin and instagram.

If you’d like to give me feedback or just shoot the shit, DM me on twitter.